Why Canadians Need to Own GOLD

Here are some of my thoughts on Why Canadians Need to Own GOLD and I’m talking physical, hold it in your hand gold. First off, this isn’t a doom and …

Here are some of my thoughts on Why Canadians Need to Own GOLD and I’m talking physical, hold it in your hand gold. First off, this isn’t a doom and …

Are you people putting money to work in these crazy markets? In this post I discuss where I see value and where I’m putting my money to work. Asset Markets …

How Average People Get Rich is really quite simple, but few have the dedication to achieve it. If you think you’re one of those people then keep reading. For years …

Are you ready for 2024? I think 2024 will Be A Great Year to Grow Your Wealth! Hey everyone, hope you like the new look of the website. I think …

What an age we live in! We live in age of extremes. A time where various trends and forces are pulling apart the fragile political, economic and social structures that …

It’s October and markets are falling hard. Usually I’d start by discussing how stocks are tanking, but what’s even more concerning is that it’s global bond markets that are selling …

Is this Global Banking Crisis 2.0? The global economy faces a major crisis that is rarely discussed or debated but rears its head from time to time in the form …

We are finally mortgage free and believe me, there is no greater satisfaction than having a paid off home! This is a major step on our road to financial independence. …

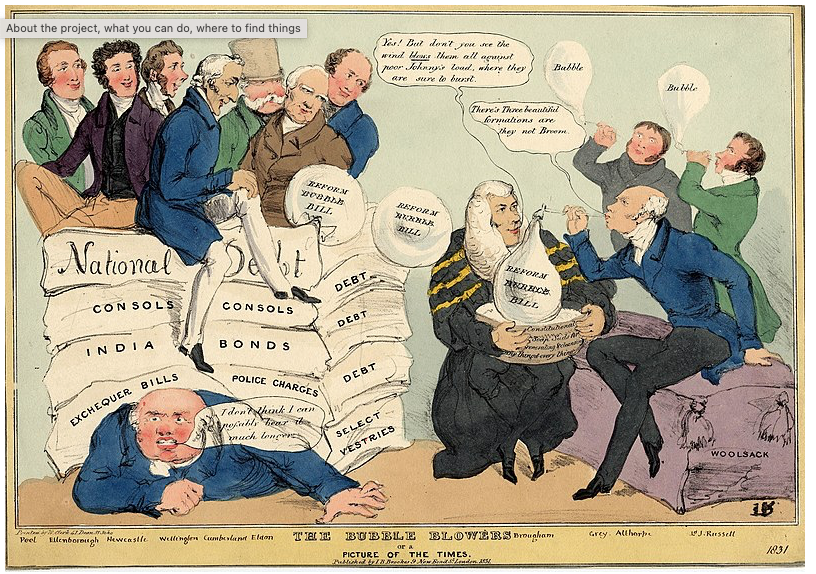

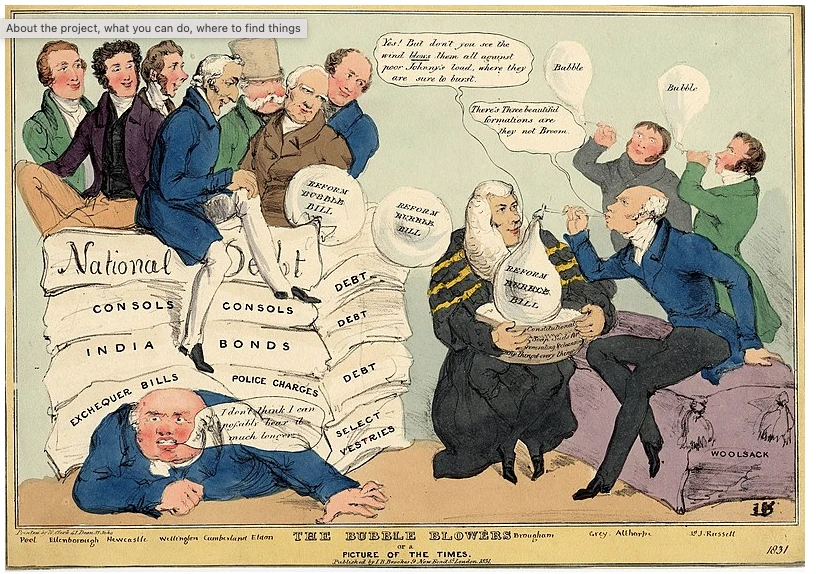

Will Rising Interest Rates Pop Global Debt Bubbles? Yesterday the US Fed hiked its key overnight interest rate by 0.75% and said more hikes are on the way as Central …